In today’s consumer landscape, financial institutions face myriad challenges managing credit and debit card fraud. This can range from high decline rates, rising fraud schemes, and an uptick in false positives, adversely impacting an institution’s bottom line and creating fractures in account holder trust.

SRM has created a multi-faceted, proactive, and comprehensive approach to institutional fraud management, which targets fraud at its core and strategically outlines a success plan.

A credit union with an asset size of over $3 billion approached SRM with two pressing challenges. The first was a surge in fraudulent transactions, leading to an overflow of dispute cases, write-offs, and dissatisfied members. The second was the delicate balance between preventing false negatives and approving legitimate transactions, a struggle impacting their operational efficiencies and member experience.

Acting quickly, SRM conducted a data-driven analysis that meticulously evaluated the credit union’s fraud detection and prevention process across the entirety of the authorization life cycle. The assessment process included and compared the credit union’s current risk rules across various product offerings, setting a benchmark for effectiveness.

A thorough review of the credit union’s current tools and techniques for fraud management, including in-house solutions and third-party providers, set the baseline for SRM’s assessment. SRM also evaluated triggers such as parameter settings, alerts, and notifications, in addition to operational procedures for handling instances of fraud.

SRM took a collaborative approach, engaging in specific review sessions with the credit union’s leaders and its network, processor, and dispute management solutions providers. This cooperative effort was instrumental in identifying potential solutions based on effectiveness and seamless implementation. SRM also provided detailed recommendations, guiding the credit union to optimize card product setup, enhance authorization processes, and implement operational best practices to reduce fraud while balancing declines from false positives.

As a result of the fraud management assessment, SRM identified fifteen high-impact recommendations to reduce fraud losses and optimize customer authorizations. SRM outlined initiatives such as declining transactions that fail essential verification checks, including name, card number, expiration, and CVV. Most notably, SRM recommended that the credit union implement the randomization of card numbers across all BINs to enhance security measures and to prevent systemic attacks on BIN fraud instances.

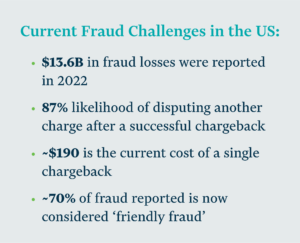

The credit union was also grappling with an influx of customer disputes stemming from an uptick in fraudulent transactions. As a result, the credit union determined that they needed a more effective approach to dispute handling to minimize financial losses and maximize successful chargebacks.

SRM addressed this issue by conducting a dedicated assessment of disputed transactions. By profiling each case, SRM was able to identify patterns and common characteristics within the existing dispute resolution process and third-party service solutions. SRM carefully examined resolution rates and charge-off instances to identify weaknesses in the credit union’s current approach and how technology handled disputes and chargebacks.

Leveraging data-driven insights, SRM produced a tailored strategy to maximize successful chargebacks and significantly reduce charge-off rates. SRM identified inefficiencies, bottlenecks, and areas contributing to losses. The result was a refined workflow for all the above challenges.

Ultimately, SRM created several recommendations to enhance servicing, including the effectiveness of affidavits for disputes in minimizing friendly fraud and the implementation of a goodwill policy for disputes less than $25 under certain criteria.

The final assessment SRM performed was related to managing customer servicing across touchpoints and card lifecycle stages. SRM’s assessment took a comprehensive review of the member journey and key touchpoints, including channels such as IVR, call centers, online and web, mobile, and in-branch interactions. This review looked closely at existing servicing capabilities in addition to feedback garnered from surveys and Net Promoter Scores.

Based on the assessment, SRM also guided the development of a member plan that aligns with industry best practices, focusing on capability gaps regarding people, processes, products, data, and technology.

As a result, SRM identified 20 high-impact recommendations that strategically improve service. The most practical recommendations included establishing a unified contact center approach for disputes to streamline communication with cardholders, simplifications to new member onboarding, and adoption of a single application and underwriting process for their credit card products.

SRM’s dedicated fraud experts were able to analyze, strategize, and execute an effective strategy to improve the credit union’s fraud management, reduce charge-offs, and increase service efficiency in only four months. The credit union is actively utilizing the success plan SRM provided and is experiencing significant operational improvement.

To view a printable version of this case study, click here.

Contact us and see how our experts can unlock savings, efficiency, and innovation for you.